The Little Yield Curve Inversion Who Cried Recession

The Little Yield Curve Inversion Who Cried Recession

"It is impossible to begin to learn that which one thinks one already knows." ~Epictetus

Disclaimer: I am short long dated treasury ETF $TLT (thesis is here). Saying that off the bat as this article is a byproduct of that research. Also - I have skin in the game so if my thinking is flawed I would be pleased to find out. This is not investment advice - DYODD.

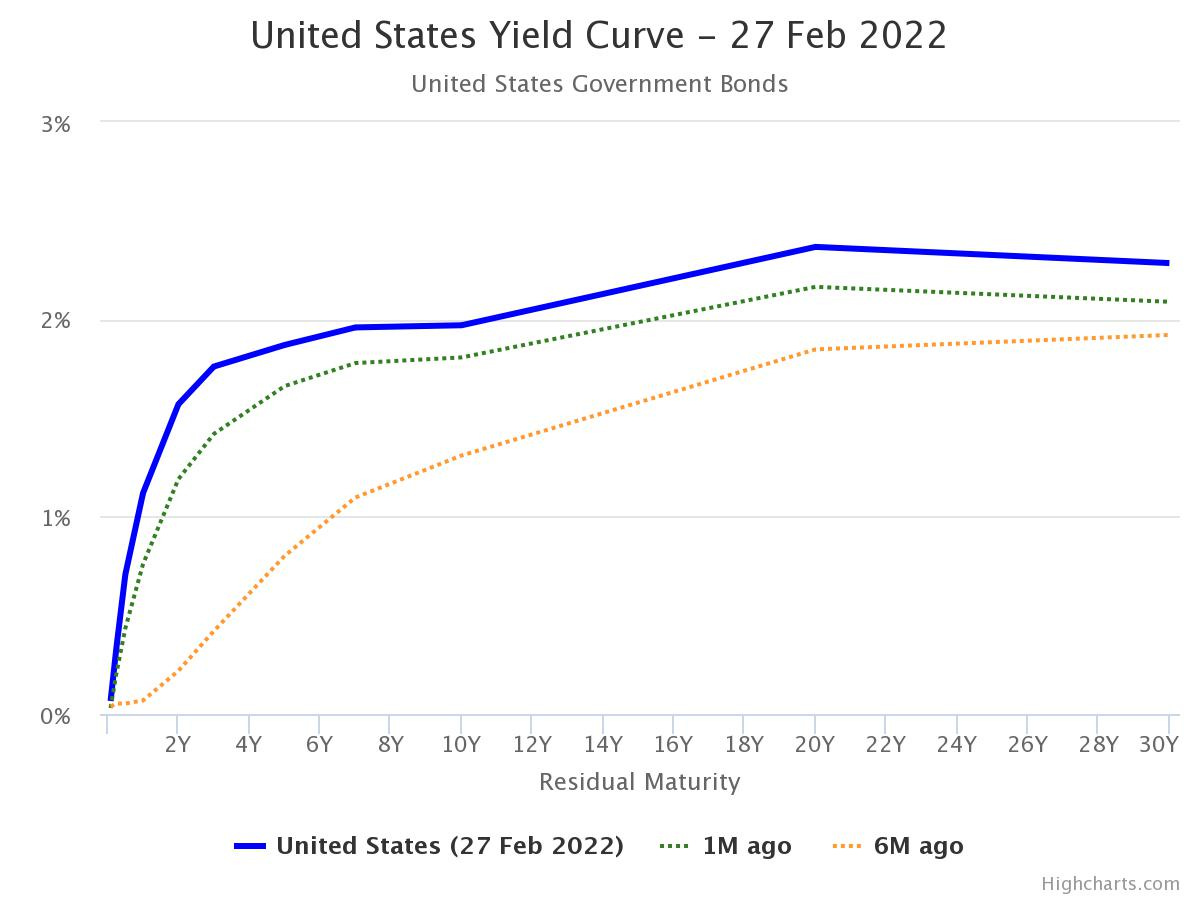

An event horizon seems to be looming. The event is known as a ‘yield curve inversion’ and its horizon is the U.S treasury bond market. It officially arrives when both the 2 year and 10 year treasury yields match, and this moment has been known to curse the future ahead of it by quite dependably predicting recessions which follow in 18 months or so. Therefore, with another one on the horizon as I type (2yr at 1.57%, 10yr at 1.97%) people are understandably grasping their bells and sounding the alarm; “Here ye, here ye, recession is nigh!”

But I’m saying, maybe not so fast with that handbell, good sir.

We’ve already seen the yield curve invert in August 2019 - over 30 months ago. But only 7 months into its 18 month doomsday countdown, a global pandemic rudely disrupted the world and scrambled the clock. Our systems were thrown into re-calibration. Here is my shortest summary of the events that followed:

Supply shuts down momentarily. Demand halts momentarily. China immediately gets to work to return to moderate supply. The US just as quickly warms up the printing press to moderate demand (or stimulate demand, 25% of GDP you be the judge). Rates go to nil, citizens get stimulus and the Fed starts buying $120 billion in bonds monthly. We bobble (more like bubble!) down this lake of liquidity for 2 years. Until now. We have hit turbulence. Inflation hits a 40 year high of 7.5%. The Fed is poised to respond with their plan to tame inflation - even as Russia invades Ukraine - to exit the bond market as a buyer in March, begin raising the Fed rate and tighten further if needed by selling bonds. This plan is by urge of the U.S people, the U.S Government and by the principles of their only two mandates. Full employment: Check! Price stability: … Write a cheque?

But the yield curve is flattening! Doesn’t that mean recession is imminent? Why is the Fed hiking and tightening into a recession? Oh dear God no the dreaded curse!

Easy with that bell still, please. This signal today (p.s signal hasn’t happened yet) assumes either the first alarm from 2019 is still accurate or the curve in 2022 is sending accurate signals, or both. But I would argue that neither, let alone both, are slam dunks:

a) I wonder if the first alarm in 2019 is no longer accurate for our moment now. A global pandemic and its response has substantially altered our markets, economy and people. Trillions of new dollars have entered our system. Asset bubbles have grown in markets that didn’t even exist in 2019. Serious inflation is effecting broad areas of the economy, beside a dam of lending capacity plus stock market liquidity. Demand for housing is strong and supply is at record lows. Supply of food and energy just got a whole new level complicated, graduating from the class of ‘supply chain disruptions’ to the class of ‘cold blooded war’. With crucial elements for both being supplied (or now, not supplied) by the very countries at war. Meanwhile, U.S consumer spending increased in Jan and the top half has an extra $2.5T in excess savings whilst the bottom half are reviving unions to fight for wage increases. My conclusion? We’re not in 2019 Kansas anymore.

b) The current yield curve might not be saying anything at all. The front end of the curve is captive to what the Fed does with their funds rate which is basically controlled by the Fed’s rate move predictions (see the FOMC dot plot below):

While the back end seems to be far less liquid and far less informative. Why? The Fed has been buying in the bond market for 2 years and possibly significantly weighing down yields, especially at the long end. Come March they wont be buyers. The new issuance coming to market will be priced by the market with no Fed backstop - and then I will be listening closely to hear what the curve has to say.

We’ve already got a few ‘blues clues’ however:

Clue 1. What are dealers in the bond market willing to pay for treasuries right now? Bob Michele (fixed income chief at JP Morgan) told us here. He’s preparing for 10 year yields to rise as high as 3% this year.

Clue 2. What is the Fed’s intention on how to impact the yield curve? Esther George (Kansas City Fed President and voting member) told us here. James Bullard (St. Louis Fed President and voting member) told us here. Basically, they have the option to sell the bonds on their balance sheet back to the market forcing the long end of the yield curve up without needing to touch short term rates. This will make lending for houses more expensive and reach-for-yield behaviour less favourable. Oh, and they plan to hike rates but won’t commit to how many, consensus is every meeting up to 5-8 times.

Yeah whatever Hawkes, talk about crying wolf! The market seems to think that Fed tightening will cause themselves to throw a tantrum (just like in 2018) and the Fed will turn straight back into weak little doves. If the Fed members words were all we had to rely upon, I might agree. But in 2022 inflation is high and must be addressed. This means the Fed has to prioritise the real economy over the markets, making pivoting back if/when markets freak out not as simple as it once was.

So it matters to not just take your cue from a yield curve but more importantly, understand:

what’s happening in the bond market

inflation

how inflation effects bonds

our real economy from the broadest perspective

Although I lean towards inflation or stagflation as the reality for the U.S, dire circumstances could spell recession. Recessions mean flight to safety of fixed income, but considering bonds are already paying negative real yields a flight to this asset would call for pretty dire circumstances (nuclear war would probably suffice). So let’s open up our minds to the possibility of either:

Recession

The economy is slowing down and demand is reducing

Go long bonds, fixed income and cash

Inflation

Too much demand chasing too few goods resulting in increased costs

Go long commodities, inflation-protected assets and stocks with pricing power

And if you’re us, short bonds!

To evaluate which is more likely, the below questions are a good place to start:

How strong is the U.S economy?: How much excess savings do people have? How are consumers spending? Is the housing market hot? How much is lending being held back by restricted supply?

What is the outlook for cost-push inflation? Is supply restricted? Have the shipping issues been resolved? How’s production input costs tracking? How will disruption to fertiliser/wheat/gas from the war effect the inflationary outlook?

Whats the outlook for demand-pull inflation? Is demand strong? Hows consumer sentiment?

At what point does inflation become entrenched or expectations become unanchored? At what point does it begin changing psychology and behaviours? Has that already started to happen?

Conclusions over to you, but if an inversion does occur in the next short while - can we depend on our little yield curve inversion who successfully calls recessions, or might it be crying wolf this time?